A house security credit line (HELOC) and a house equity loan one another provide bucks because of the accessing the equity you really have of your home. In the two cases, the eye charge are taxation-allowable. It normally keeps a beneficial 10-season period of time where it is possible to make brings doing the borrowing limit; the next ten-season period ‘s the cost period. A home collateral loan along with uses your property equity, for the amount borrowed distributed to your just like the a lump sum instead of a credit line and you may usually has a predetermined interest.

An economic coach help you decide in the event the a HELOC is good for you. Discover one easily, use SmartAsset’s 100 % free advisor coordinating unit today.

Tax Rules and you may Household Security Write-offs

The brand new Income tax Cuts and you can Work Work is actually passed effective , and you may mandated sweeping income tax change. Domestic guarantee money, such as the HELOC, while the tax deductibility of its desire charge was indeed impacted. The fresh taxation aftereffect of the law toward HELOCs or any other family guarantee loans was to reduce tax deductibility of great interest so you can the method that you spend the financing.

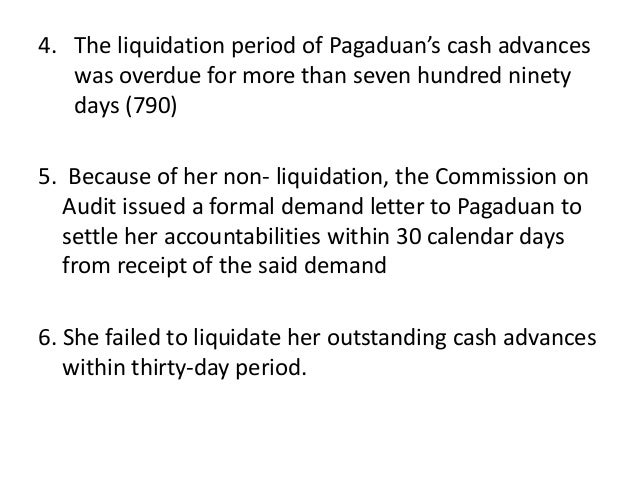

Towards the attention charges to get tax-deductible, brand new continues of one’s credit line must be allocated to the property that was useful equity. The brand new tax code says the mortgage should be spent to pick, generate otherwise considerably increase the home on what the new personal line of credit would depend. The eye is actually allowable if you are using the new continues to help you upgrade your residence. Here is the laws up until the Taxation Slices and you can Services Act expires inside 2026.

Unless you itemize deductions, the interest you only pay to the an effective HELOC is not going to help you. Fewer folks have itemized as the income tax reform due to a greater basic deduction. To possess 2022, the standard deduction was $twenty five,900 to have married people filing as one and you will $a dozen,950 getting single anyone. Considering the large basic deduction, itemizing may possibly not be advantageous to you. Therefore, the eye you have to pay, even for property recovery, into a great HELOC will not be allowable.

New Deduction Constraints

Since the 2018 taxation change rules, the fresh new tax deductions restrictions provides changed towards the all financial and household guarantee loans. You might only subtract attract costs to your a maximum of $750,one hundred thousand into the home-based loan financial obligation and HELOCs whether your type of credit are approved ahead of . In case the HELOC was accepted in advance of one to go out, it’s also possible to fall under the existing maximum off $one million. Consult with your income tax mentor to ensure.

Up until the 2018 rules, you might only subtract all in all, $a hundred,000 home based collateral loans. But not, you can need that deduction no matter how you had been heading to blow the https://elitecashadvance.com/loans/direct-deposit-loans/ bucks from your own HELOC otherwise home collateral mortgage. They did not have to be just on assets renovation. Today, you’ll be recognized getting a beneficial HELOC for many different causes including household home improvements eg settling highest notice personal credit card debt otherwise funding a degree. Although not, focus write-offs can not be taken for those intentions.

Advantages of Taking out a great HELOC

Once the pandemic, HELOCs and you may house equity funds had been more challenging to acquire. Actually, a couple of major financial institutions, Wells Fargo and JPMorganChase prevented recognizing applications to them altogether owed to market criteria. In the event the HELOCs grow scarcer, the money-aside re-finance marketplace is gonna grow.

Although not, whenever you rating an excellent HELOC, you will find gurus not in the attract deduction. Such as, you only pay attract simply on the level of the new HELOC you to definitely your draw down. When you get a home equity financing, you pay appeal on the earliest with the a huge lump sum. HELOCs save you money. You additionally usually have a ten-year time frame in advance settling the main. Inside earliest ten years, you simply pay back interest.

Just like the a beneficial HELOC was a credit line, you borrow only what you need when you need it. Particular loan providers have begun offering a predetermined rate of interest towards the HELOCs, with usually carried a changeable interest rate. There are also pair restrictions regarding how you need to use HELOC finance. Accessing the amount of money away from a beneficial HELOC is sometimes as simple as composing a check.

Realization

HELOCs are good for customers that are self-disciplined to make on-day repayments. But not, you must keep in mind that whilst great things about an excellent HELOC are many, there are even disadvantages. Youre experiencing your residence’s equity and you may placing your home at risk whether your money falls, you eradicate your job or some other knowledge that you are unable to expect happen. The interest rate towards an excellent HELOC are adjustable, very when you look at the a promising interest ecosystem, an excellent HELOC is almost certainly not a beneficial economic choice.